Small catering companies declare a profit of 129 euros per month. Hairdressing salons €162 on average and bars €188.3 per month. In bakeries, the average monthly profit is 280 euros and in retail clothing stores, 294 euros. In taxis, the amount reaches 307.7 euros per month, and in flower shops, 380 euros. The plumber does not exceed 500 euros and the electrician 574 euros per month. The largest “monthly” among self-employed workers is shown by the pharmacist (with 1,726 euros per month) and the doctor with 1,661 euros. The €1000 barrier is barely “broken” by 8 professional categories in a total of more than 550.

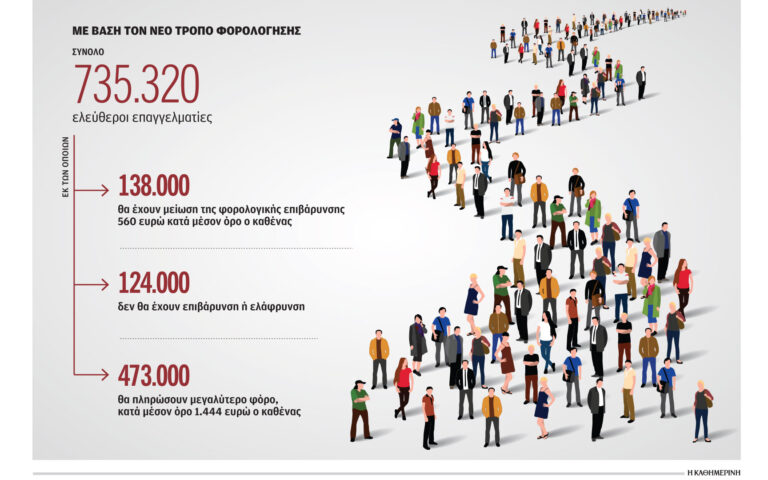

Online database used by the government and Ministry of Finance The design and cost of the new tax method for more than 700 thousand taxpayers was based on what the specialists declared in their tax returns. In the summer of 2024, the data will be officially published through the AADE website, where in particular gross income will henceforth be an essential element in determining income tax. Items that Edited by “K” They reveal:

1. In a total of 534 two-digit activity code numbers into which 642,128 individual enterprises are classified, the average profit is €8,165, i.e. €680 per month. If the average income tax is also deducted, a net monthly income of 618 euros is obtained, i.e. less than the net salary of an unskilled worker (about 667 euros).

2. Among 534 professional branches:

• 44 declare annual net profits of less than €3,000. About 68,000 specialists are active there.

• The 74 companies show annual net profits of between €3,000 and €5,000. There are 145,731 professionals here.

• From 5,000 to 10,000 euros annual earnings declared by 190 professional categories (KAD) in which 222,264 professionals are classified.

• From 10,000 to 30,000 euros per year – always on average – declares 213 branches of professional activity comprising approximately 206,000 professionals.

• Only four sectors show an average annual net profit of more than €50,000 and they include… 39 professionals.

3. Approximately 179 CAD have been identified that display a single number Profit marginIn several cases, less than 2%. Small profit margins are partly justified in retail, but the list of very low margins also includes occupations classified as providing a service such as restaurants. A single-digit profit margin means that expenses are equivalent to between 91% and 99% of income, or that for every 100 euros of income there is a profit of between 1 and 9 euros at most. At the other end of the scale, higher profit margins of over 30% were reported in Greece with a maximum of 106 departments, mostly in the services sector.

The published table classifies professional activities according to the number of assignees. Each professional is classified into a specific KAD as long as he declares the highest income for the year in it (note that a professional may declare more than one activity code on his own initiative). The average, by definition, does not give a clear picture of the ranking positions: that is, how many advertised earnings of less than €1,000 per month and how many exceeded this threshold. However, it gives a clear picture of the levels at which each branch moves.

Only four sectors show an average annual net profit of more than €50,000, and they include… 39 professionals.

What comes out?

• The largest number of professionals carrying out legal activities: 33,884 PINs. Average revenue is €23,320 and average profit is €12,582. Profit margin 54%.

• The four-digit KAD 5610 (Catering Services Activities) is offered as a major by approximately 29,902 professionals with an average income of €90,763 and an average profit of €5,509. The industry profit margin is 6%.

• Taxi operators (KD 4,932) are the third largest group with 27,195 professionals, with an average income of €16,783 and an average profit of €3,692 per year.

• Engineering activities and technical consultations, the fourth session of KAD. It has 26,053 professionals with an average revenue of €30,487 and an average profit of €13,716 or a profit margin of 45%.

• KAD 5630 Integrates Bars (Beverage Service Activities). The specific occupation is declared by 25,071 professionals, and although they show an average income of €42,291, they limit the average profit to €2,259 and the profit margin to 5%.

• Followed by private medical professions (8,622 Kuwaiti dinars), which includes 22,593 scientists who declare their average income to be 44,240 euros and an average profit of 19,937 euros, bringing the percentage again to 45%.

• Holiday accommodation in Greece generates an average annual profit of €7,450 based on tax returns of 17,893 professionals who declared turnover of €35,524.

• In eighth place in the ranking based on the number of professionals is KWD 9,602, which includes barbers and hair salons. The country has 16,127 individual enterprises in this sector with an average income of 15,648 euros and an average profit of 1,947 euros. The department also generates an average monthly income of €162.

• The 9th most populated place is 6,920 KAD with 16,079 representatives who declare an average income of 27,207 EUR and an average profit of 9,854 EUR or a profit margin of 36%.

• The top 10 is completed with other human health activities with 13,900 professionals, an average income of €21,300 and an average profit of €8,273 or a profit margin of 39%.

The “key” is the average trading volume per branch

Data on the average annual turnover of professionals for each activity code number will be officially published on its website Independent Public Revenue Authority So that professionals can access and know whether or not they will be burdened due to the amount of their income. The draft law stipulates that publication be made within one month of the deadline for submitting income tax returns. Under the amended provision, the additional sales fee would be 5% of the amount by which the obligor’s sales volume exceeds the average annual turnover of the CPA at which the obligor generates the highest revenues. These additional fees will not apply when:

1. The average annual trading volume of the corresponding KAD does not exceed 10,000 euros (these cases are very limited and do not exceed 15-16).

2. When the number of occupations falling under the specified KAD does not exceed 30 (it is estimated that there are at least 170 KAD or approximately one in three classified in this category).

Low profits and small profit margins bring burdens

The new tax calculation mechanism targets professionals who declare the lowest profits and also the smallest profit margin. The less earnings appear on the most recent tax returns, the further away from the minimum income the formula will be, and thus the greater the burden. Those who declare income greater than the average for their industry will also have a greater burden. Based on actual data obtained from tax returns, the following examples are typical:

1. A taxi operator who declares annual sales of €26,783 (i.e. €10,000 above the industry average) but makes profits as much as the industry (i.e. €3,692) will find itself ultimately taxed on a profit of €14,696 instead of €3,692, which is This means that he will pay income tax of 1,933 euros and not 332 euros as is the case now.

2. An electrician who would show an income of 86,276 euros (instead of 36,276 euros which is the KAD average) but profits as much as the sector (i.e. 6,891 euros) would end up being taxed on a profit of at least 16,696 euros, with a tax of 2,371 euros.

Higher taxes will also be paid by those who declare income greater than the average for their sector.

With the change made by the Ministry of Finance in the final form of the bill, it has greatly reduced the impact of sales volume on the final amount of the tax. The difference in per capita income from the sector average (i.e. what is shown in the table) affects the final amount of taxable income by only 5%. The previous system (which even stipulated doubling taxable profit) made income the dominant element, with the result that hiding income (and thus not issuing receipts and invoices) became a highly profitable (and illegal) option.

Tax return data, compiled by KAD, show that the attempt to reduce the taxable material by professionals is carried out on two fronts…: the first is related to trying to hide income and the second is related to “inflating” expenses as much as possible. In 2024, activating the new tax mechanism will ensure the collection of the minimum tax for every professional, but it will not help reduce tax evasion, which affects other laws besides income tax, the most important of which is value-added tax. So the bet for the following years (i.e. 2024 will not be indicative of the bill’s performance, as there is an element of surprise since the measure also affects this year’s revenues) is not only whether it will achieve the automated projected revenues, but also what the impact will be on reported revenues and profits. .

The risk that the tax authorities will face is twofold: there will be a general attempt to “keep” declared income as close as possible to the sector average (note that the data will be published every year) and globally, on the other hand, to “inflate” costs so that “ “The declared profit is close to the minimum level required by the new mathematical formula.

In practice, the effectiveness of other measures put into effect (including mandatory electronic invoicing, linking cash registers with points of sale) will be very important, but also the willingness of taxpayers themselves to request receipts, contributing to the reduction of tax evasion.

“Avid problem solver. Extreme social media junkie. Beer buff. Coffee guru. Internet geek. Travel ninja.”

More Stories

“Recycling – Changing the water heater”: the possibility of paying the financing to the institution once or partially

Libya: US General Meets Haftar Amid Tensions Between Governments

New tax exemption package and incentives for business and corporate mergers..